Industry Performance

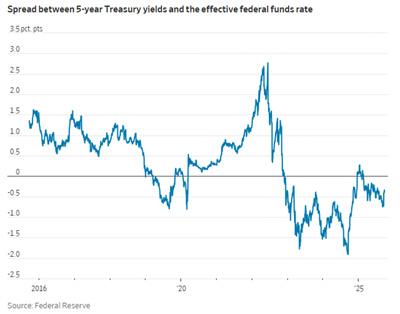

The steepening yield curve and the decline in the spread between five-year treasuries provide a lift to bank earnings and pricing. See Figure 1.

Figure 1.

Figure 1.

After all, community and regional banks are more dependent on spread and net interest margin (NIM) for profitability than their money center brethren. The relative stability of interest rates after the 2022 to 2024 explosion in inflation has enabled banks to catch up. Now with short-term rates declining, and thus, giving relief to the bank’s cost of funds, industry earnings continue to improve. Moreover, legacy loans (and even extended maturity securities) continue to roll off, and are being, and will continue to be, replaced with higher-yielding assets. In the meantime, we have been using structures to bridge the gap between fair market value and book value of underwater securities positions.

For the second quarter, community bank NIMs increased by 16 basis points quarter over quarter (QoQ) (32 basis points year over year (YoY)) to 3.62%. The median community bank return on assets (ROA) increased 15 basis points QoQ and 32 basis points YoY to an annualized 1.33%. Such improved performance is expected to continue. See figure 2.

Figure 2.

Figure 2.

Community banks achieved such performance while preserving pristine balance sheets (albeit with a few manageable cracks). Community banks ducked the large metropolitan office center implosion, thereby emerging relatively unscathed from the effects of remote work. The bankruptcy of WeWorkTM is indicative of the losses by lenders in the office tower market.

Community bank asset problems continue to remain near historical lows. Allowance for credit losses at community banks continues to be an astounding approximately 170+% of non-performing assets. Accordingly, if anything, in the short term, provisions are likely to be neutral or provide some assistance to future earnings.

The collapse of April loan demand after “Liberation Day” has subsided as businesses have had more clarity regarding the impact of tariffs. Consumer spending has continued to grow. Despite the slack in the economy, such spending provides encouragement that businesses will, at some point, need to catch up with investment activity. Even in the current environment, the likelihood of avoiding a recession (the Atlanta Federal Reserve Bank continues to forecast growth around 2%) makes lending more predictable.

Community bank loans increased 1.7% QoQ for the second quarter (4.9% YoY). Loans were up in almost all categories except C&I. Banks continued to grow core deposits while shrinking brokered deposit levels.

Regulatory approval

The regulatory environment has also helped to increase bank M&A activity. For existing strategic acquirers, the speed with which regulatory applications are being approved, as compared to the glacial pace during the Biden administration, means that buyers do not need to be concerned about preserving their approval capacity for the one perfect deal. Instead, they can consummate one transaction and then return to the market.

The Trump administration’s warm embrace of cryptocurrency, as well as perceived openness to Fintech ownership and more technology-forward banking, has led to a stampede of potential entrants into the marketplace. In addition to new bank charters, many of these players are looking to acquire existing institutions. We represent a number of these “new” buyers. The willingness of such institutions to pay up for potential early entry has led to banks of less than $250 million in assets selling for higher prices (1.63x tangible book value at June 30) relative to larger institutions.

Public Pricing

The combination of these factors has lifted the market value of bank stocks. In September, the KBW Regional Banking Index showed signs of catching up to larger banks. Whether it is because of sector rotation, a concern about forward p/es of the S&P 500, improved industry performance, or interest rate bets, regional bank stocks are up 18.38% since Liberation Day and 10.98% YoY as of September 30.

Bank stocks still trade at forward earnings multiples of only 10.9x as of September 5, as compared to a 15-year median of 12.8x. Accordingly, bank stock pricing has further room to increase.

Shift from Intrinsic to Nominal Value

Previously, buyers sought to convince sellers to engage in transactions with stock as merger consideration at lower nominal pricing (1.34x tangible book value in 2024) by touting the intrinsic value sellers were getting. In other words, buyers emphasized the portion of the ownership that the sellers were going to own. The idea was that the sellers would achieve gains as the overall bank stock market recovered.

There is still a case to be made for intrinsic value today in light of current versus historical p/e ratios. The rising value of market pricing, however, has allowed stock buyers to pay more. Through June 30th, the median bank sold for 1.53x tangible book value.

Public buyers have so far remained disciplined. They have sought to keep merger consideration levels somewhat consistent with their “pay to trade” ratio (transaction P/TBV multiple versus the buyer’s standalone P/TBV). Moreover, such firms have sought to keep tangible book value earnbacks below four years and most often closer to three years.

Efficiency Ratio and Size

The M&A imperative will continue. Banks need size to compete with the technology offerings of bigger banks. Perhaps outside of the top four banks, no others are immune from such compulsion. Bill Demchak, the CEO of PNC (the country’s 8th biggest bank), in discussing the $4B acquisition of Colorado-based First Bank, noted that smaller banks need to grow or become casualties. He indicated that he is determined to double PNC’s size to “turn his bank into a trillion-dollar” institution.

At the community bank level, the median seller had a 71.3% efficiency ratio on June 30, as compared to buyers with a 63.4% efficiency ratio. This stark difference allows buyers to achieve significant cost savings, thereby improving their own efficiencies.

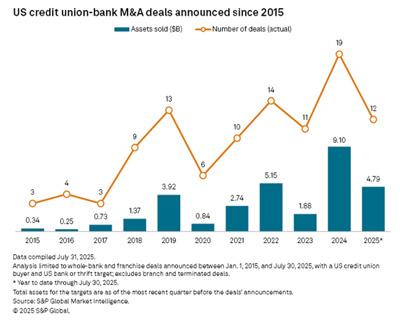

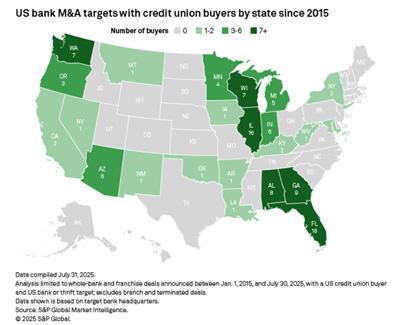

Credit Unions

The M&A story in 2024 was about credit unions and investor groups. Each of these represented approximately 25% of the deals done. Neither have gone away as buyers, but the credit union impact has diminished. Whether it is because of political pressure or higher deal pricing that makes it more challenging for credit unions to compete for bigger deals, the relative activity has shifted. In the second quarter, there were five credit union acquisitions as compared to 37 M&A deals for banks. In some states, such as Texas, commissioners have taken the position that a credit union cannot engage in a purchase and assumption transaction to buy bank assets and assume deposit liabilities. See Figure 3.

Figure 3.

Figure 3.

M&A Market

The unknown in all of these developments is pricing. Bank stock pricing is higher now than it has been in a number of years; however, the stock market has not fully buoyed bank stocks. A rising stock market tends to increase pricing overall as cash buyers need to stretch to compete.

Because of the punishing impact on buyer stocks if buyers enter deals outside the orthodoxies that have developed over the last few years, we can expect publicly traded buyers to remain disciplined. The current level of pricing allows room for cash, as well as stock buyers, to engage in accretive transactions. We can expect the pace of activity to continue to accelerate.

We have also seen a movement away from the old-style auctions. Buyers are cognizant, especially at the smaller institutional level, of the need for there to be a good fit for successful integration. Cultural issues, which are always a concern in banking, have now become part of the marketing approach of sellers.

In 2024, we represented a Columbus, Ohio bank that engaged in the highest-priced transaction (in terms of tangible book value multiple) for the year. It concluded that there was only one cultural fit and engaged in a one-on-one negotiation with an out-of-market bank. The buyer would not have engaged in an auction. We expect the focus of sellers on a handful of potential merger partners, rather than exhaust the market strategy, will continue. For buyers, it is critical to position themselves to be included in such orbits.

Expectations

M&A activity can be expected to increase further. A rebounding stock market allows the 600+ publicly traded banks to use their currency to pay higher nominal prices while still communicating attractive intrinsic value. New entrants to the market, whether investor groups or technology firms, will continue to provide demand. Credit unions have not left the market. There is always a concern that when a seller is ready to sell, there may not be enough buyers. Currently, this does not appear to be the case.